As of October 3, 2015 the mortgage loan process is changing, all part of the Dodd-Frank Act. The new loan documents can be confusing; we have decided to break the new forms down for you – page by page. If you have any detailed questions, just give us a call and we can refer you to one of our fabulous lenders. We are here to help.

Page by Page Closing Disclosure Information

- New form has 5 pages.

- It replaces TILA (Truth-In-Lending Act) and HUD-1

- One closing Disclosure is essential for each loan.

- Charge descriptions on both the loan estimate and closure disclosure must match.

- Must be given to borrower 3 business days prior to settlement.

The Closing Disclosure is now ready to replace the Truth-In-Lending Act (TILA) disclosure and the HUD-1 Settlement statement. The lender is accountable for conveying the Closing Disclosure to the purchaser, but creditors may use escrow officers to provide Closing Disclosure to the buyer or borrower.

PAGE 1

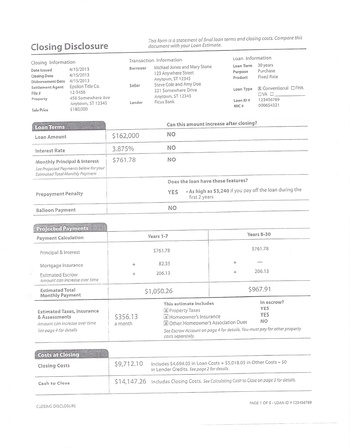

Page one is very similar to the Page 1 of the loan estimate it describes:

- Loan terms

- Loan amount

- Interest rate

- Monthly Principal & Interest

- Any Pre-payment penalty or Balloon payment

This page also procures the projected payments over loan tenure. It also reveals to the borrower what amounts will be deposited into their ESCROW account or impound. It also provides the total estimated closing costs and additional requirement of cash to close.

PAGE 2

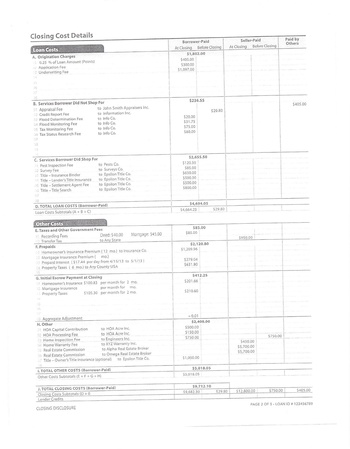

Page two is also similar to the second page of of HUD-1 Settlement Statement. It exposes all of the closing costs details and lists all loan costs which are paid by borrower seller and other third parties indulged in the loan.

PAGE 3

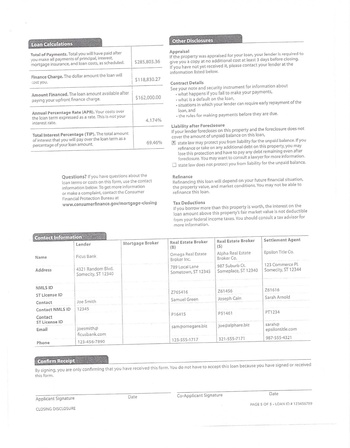

The third page shows a calculating cash table that is similar to the table on page 2 of the Loan Estimate. This table signifies the contrast among the prices levied and disclosed on the loan estimate. The remaining page shows information about the borrower and vendor’s costs and credits. It is very similar the present page 1 of the HUD-1 Settlement Statement.

PAGE 4

The fourth page encloses disclosures regarding other loan terms such as:

- If the loan is assumable

- If the loan contains a demand aspect

- May entail a late payment charge and when it may be levied

- Whether loan includes a negative paying back feature

- Whether the lender will acknowledge fractional p[payments

- Notifies the borrower that the lender will have a security interest in their assets.

This page also includes a table mentioning the charges that will be seized and how much amount will be gathered each month. To conclude the page contains flexible charges and interest rate tables if they are pertinent tot the loan.

PAGE 5

The fifth page includes information about the following:

- Entire expenses over the complete life of the loan

- Finance expense

- Amount sponsored

- Annual Percentage Rate (APR)

- Entire interest percentage detail

Under other disclosures the client will uncover information about:

- Appraisal (if pertinent)

- Contract information

- Accountability following foreclosure

- Refinance details

- Tax deductions

The bottom of the page includes contract details and signature lines. In case signature lines are integrated, the following disclosure is applied “by signing you are only confirming that you have received this form. You do not have to accept this loan because you have signed or received this form” signifying a signature is required as an acceptance of the form.

If you are thinking of buying a home and have questions about the new closing disclosures, give us a call 619.980.2738 or 619.851.4084. We are here to help!